Interview with an LP: Building (And Evolving) A Generational Fund Returns Platform

Getting the fund-of-funds perspective from VenCap International

Oper8r is focused on enabling the next generation of great founders in VC by empowering the next generation of great emerging micro-VCs that fund them.

Tell us about yourself and how we can help:

TLDR

VenCap International, a UK-based fund-of-funds, has been investing successfully in VC funds since the late 1980s with a “generational fund returns” strategy

Chris Witherspoon was one of the LP experts in Oper8r’s first cohort, and now shares his perspectives on what makes an outstanding VC

For emerging VCs, specificity of strategy and focus is critical in the near-term. Also important is having a clear vision for the long-term trajectory of the firm

Develop strong relationships with LPs - even between funds - by showing proof-points that the original strategy is actually working... or show that a new and better one is taking shape

We welcome Chris Witherspoon from VenCap International, the Oxford-based, ~$2B fund-of-funds platform founded in 1987 that has made over 300 fund commitments into VC funds in the US, Europe, India, and China. VenCap has consequently built one of the most coveted portfolios in the world.

Chris joined us in our summer cohort to share his perspective with its members. He joins us again to share his perspectives.

Chris, we're delighted to have you again! To start, tell us a bit about yourself and your firm

Thanks Welly. Brief background. I hail from Gateshead in England - I share this honor with Brian Johnson, the lead singer of AC/DC. Needless to say, one of us took the more exciting career path (sorry, Brian!). I spent the early part of my career at KPMG - between the UK, Hong Kong, Middle East, and South Africa - before joining the British Business Bank to focus on emerging VC, then to VenCap, where I have spent the last four years.

VenCap is a VC-focused fund-of-funds based in the UK. We’ve been investing in VC funds since the late 1980s. During that time we’ve been incredibly lucky to have indirect, early-stage exposure to category-defining companies including Amazon, Google, LinkedIn, and - more recently - Zoom, Pinduoduo and Snowflake.

Who are your LPs? What are your LPs trying to optimize for?

Our LPs are a mixture of pension funds, family offices, and endowments primarily based in Europe. Across this group, there are different investment strategies being executed. However, one prevalent theme is that they are looking for exposure to the next generation of market-leading businesses, and believe that the vast majority of these will emerge from the VC industry.

Our current strategy (linking back to your recent article looking at LP motivation for investing in Emerging VCs) is most similar to “generational fund returns” in that we back a concentrated group of firms that have demonstrated an ability to identify and access those outlier companies that drive returns for the entire industry, and show potential to do so across multiple funds. These funds invest primarily in the US, but also China, India, and Europe – reflecting the global nature of VC in 2020.

What does success for a “generational fund returns” strategy look like for you?

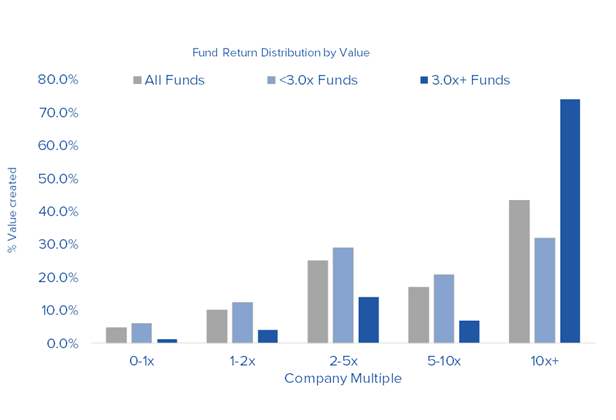

We’re fortunate to have a relatively large data-set covering 322 funds and more than 12,000 companies.

One of things we’ve observed over that length of time is that VC is a pretty tough business! As an example, more than half of all underlying portfolio company investments lose money. Our data shows that even the very best funds lose money on north of 40% of deals.

What separates great funds from the crowd is less the ability to avoid losses, and much more to find a company, or companies, that return 10x cost or more.

This chart, which shows where the value in a fund has been created across our early-stage portfolio from 2001-2014, brings this point into focus. More than 70% of ALL of the value created by 3.0x net funds comes from individual companies that returned 10x cost or more.

What do you normally look for in an established VC?

Our aim is to construct portfolios of funds run by investors that operate with a “fund returner” mindset. We’ve found this to be a successful formula for delivering consistently strong returns to our LPs, vintage in, vintage out.

However, it is important to note that whilst having a fund returner in the portfolio is essentially a prerequisite for outperformance at the fund level when it comes to early stage investing, fund returners come in many shapes and sizes, particularly as it relates to portfolio construction:

Single digit initial ownerships through to north of 20%

Less than 1% of committed capital invested in a fund returner up to 17%

Exit ownerships ranging from less than 2% to 50%

In other words, we’re looking for early stage funds to swing for the fences, and recognize that these swings can look very different, so are agnostic as to which technique is pursued to achieve that.

Over and above the potential for outperformance, we expect to commit to VCs over the course of multiple funds - a “generational” relationship - so we want to back firms that are building for the long-term.

Our strategy is not suited to backing managers that are looking to capitalise on a short-term opportunity over building a long-term franchise. It’s one of the reasons we’ve tended to steer clear of funds that expect to focus only on a single sector or technology over the long-term. Given that trends have a habit of fading, we need confidence that the VC will have a strategy that will outlast the trend.

What do you look for in emerging VCs that’s different from established VCs?

We typically think of any firm that is on its first three funds as emerging. We also expect that the managers have sufficient investing experience to let them weather various market conditions, or at least a team around them (e.g. advisors) that can help them with this.

We apply the same set of criteria to the assessment of an emerging manager as compared to an established group. The difference lies in the availability of data, both qualitative and quantitative, upon which to base an assessment. Therefore, we’re looking for proxies that would point to an ability to identify and access future fund returners. This is a likely to be some combination of:

Evidence of a network with the potential to produce exceptionally high quality deal-flow. Some of the types of individual who tend to be best placed to demonstrate this include:

Former tech entrepreneurs

Early employees of breakout tech companies

Individuals who have carved out a reputation at more established VC firms

Positive “off-list” references from others in the relevant ecosystem including GPs and LPs - especially within our network

Track record from Angel investing and/or prior firms with an emphasis on quality over quantity, i.e. letting your schedule of investments demonstrate that you are able to recognize actual or potential fund returners

Regarding potential fund returners, these may be companies in the existing portfolio that, whilst they may not yet be stone cold winners, carry the hallmarks of becoming a category-defining business (e.g. established VCs with long histories of capturing fund returns are consistently following your deals)

One area we over-index on relative to an established firm is vision with respect to how the firm will evolve. We’ve had some very positive experiences with firms that have started small but had a strong view on where they wanted to be in the medium to long-term. There are many examples of firms- now considered amongst the strongest Silicon Valley early-stage investors - that started with a very narrow focus, but had a clear vision for how to expand on it.

What should emerging VCs be doing differently?

As you highlighted in your previous article, LPs have different motivations, goals and strategies that drive their attitude to VC.

Putting the time in to understand what motivates LPs you believe would be a good fit for your strategy and catering your message to your audience will pay dividends, which is why I think the data that you are collating and sharing at Oper8r is incredibly useful – it helps both VCs and LPs execute their roles more efficiently.

Also try to build relationships with LPs when you are not fundraising.

Mark Suster wrote a blog post several years ago talking about investing in lines, not dots. We think that principle can also be applied to LPs. Part of my job is to demonstrate that a firm has made real progress against its strategy and vision, and should belong in our portfolio. As an emerging VC, you can help me with this by sharing those proof-points along the way.

Chris, thank you again for sharing your expertise!

My pleasure!