Analysis: The LPs That Invest In Emerging Micro-VCs

Are established VCs the new funds of funds?

Oper8r is focused on enabling the next generation of great founders in VC by empowering the next generation of great emerging micro-VCs that fund them.

Tell us about yourself and how we can help:

First: Thank you! We are so grateful to the many members of the emerging micro-VC community (including self-reporting LPs) that have already contributed data to this open initiative.

Even though it has been less than a month since we asked about who invests in emerging micro-VCs, we feel we have enough data to start making some observations.

A note on methodology:

All data comes from public or self-reported sources

We sourced data through internal research and external submissions

We accepted names of organizations (not individuals)

Investors in only emerging micro-VCs (generally fund I/II, <$50M-ish AUM) in the US

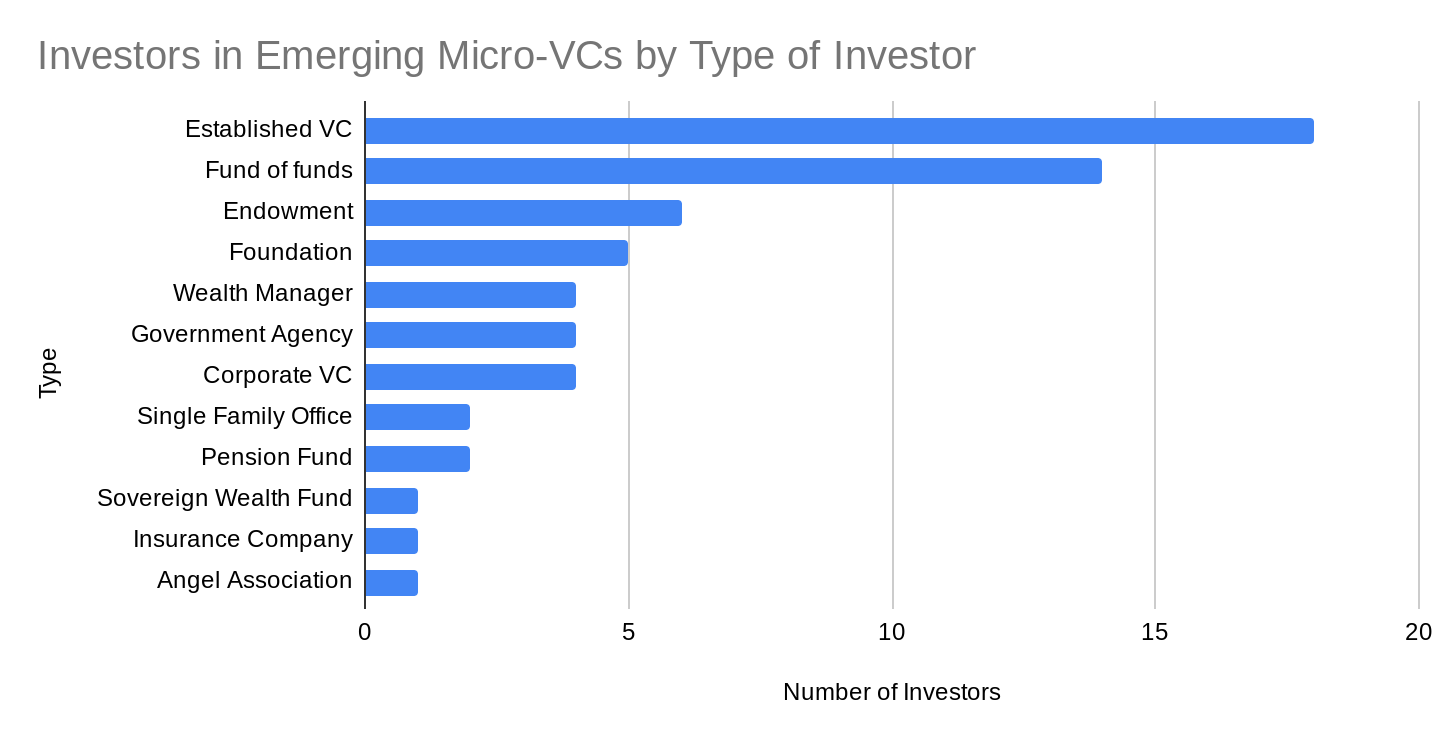

OK, here’s a summary of the data as of today:

A few observations:

37% of the investors are actual institutions (endowments, foundations, etc.)

29% are intermediary allocators (funds of funds and wealth managers), channeling capital from institutions and wealthy families/individuals

34% are wealthy families and individuals (family offices, an angel group, and established VCs - assuming that commitments are coming from the individual GPs, and not the funds themselves)

That said, it’s important to remember that the majority of LPs into micro-VCs are family offices and high-net-worth individuals (HNWIs), and institutions do make large commitments, but they’re rare.

In other words, an institutional LP like the Harvard endowment committing to emerging micro-VCs are a bit like an established VC like Sequoia investing in a pre-seed startup. Does it happen? Sure. Should you celebrate if it happens? Absolutely! But is it likely to happen? Probably not.

So in the spirit of thinking about product/market fit where a fund is the product, and the LP is the market, we’ll spend more time looking at the types of investors that are actually in the market, and what motivates them to invest.

Also, we will start tracking the organizations affiliated with HNWIs (i.e. where they made their money) so we better analyze the sources of capital, and motivations for the commitments.

Note: For HNWIs, we will be using the name of the affiliated organization rather than the individual’s name, and will add a new investor-type to indicate that the investment is coming from the individual rather than the organization.

Thank you again for contributing!