Benchmarks: Demystifying VC co-investing with data from >5,000 SPVs

It’s… specialpurposevehiclisticexpialidocious!

Oper8r is focused on enabling the next generation of great founders in VC by empowering the next generation of great emerging micro-VCs that fund them.

Tell us about yourself and how we can help:

TLDR

Happy 2021!

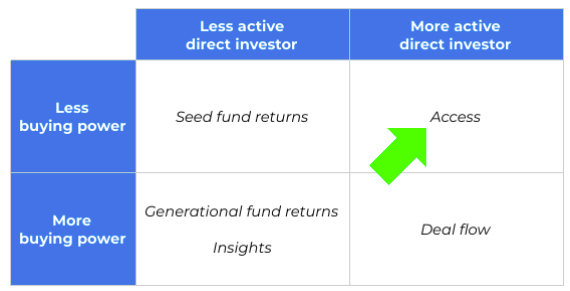

“Pro-rata rights… is a hidden asset” for emerging micro-VCs (with the access) and LPs (seeking the access) into breakout startups, making co-investing a core motivation for LPs to invest in emerging VCs

Combining a blind pool with discretionary co-investments results in a “blurry vision pool” strategy that lets LPs maintain discretion, VCs increase AUM, and both to build a relationship

Although there are many reasons for co-investing in emerging VC, there is little hard data on what co-investing looks like, so we asked Assure to share what they are seeing across the 5,000+ SPVs on their platform

We share those benchmarks, observations on what the data mean, and thoughts on how emerging VCs and LPs can use the data

We Care About Co-Investing With Emerging VCs

I get excited about co-investing for emerging micro-VCs because it brings together a few points we covered previously:

A small fund typically means having to write small checks, which means having to invest early, which increases the potential for outsize returns

Micro-VC funds alone generally aren’t a significant source of revenue, so emerging VCs need to be creative about how to make the most of a small capital base for their LPs

Co-investing is one of the reasons (“Access”) that sophisticated LPs prefer to invest in emerging micro-VCs

It also relates directly to one of the inherent realities for many emerging micro-VCs, which we described in that last article:

...micro-VCs tend to be allocation-rich, but capital-poor. In other words, it’s hard for emerging VCs with small funds to reserve enough capital to exercise pro rata in their best companies round after round. If you are an LP that is far outside the VC ecosystem, however, you likely have the opposite problem... which makes for a potentially perfect pairing!

Or as an experienced VC described the value of early-stage VCs:

• When early stage funds help create companies, they receive the right to continue to invest and maintain their stake (“pro-rata rights”). This call option on growth investment in their best portfolio companies is a hidden asset.

• Early stage VCs are long time board members in these companies, so they know them well. They have the best opportunity to spot the true winners and put the fund’s capital behind them.

But Is There Enough Data To Do It The Right Way?

There is a lot to say about co-investing, and a lot that has been written about it already - generally, these are along the lines of why it’s a good idea, why it’s a bad idea, how to do it. In fact, our very own Winter Mead wrote about the topic in 2015.

But I haven’t yet seen anyone go into the actual numbers around VC co-investing, and specifically as it relates to the basics around how much to raise, how much to charge, or how long to wait.

And the timing feels right because one of my favorite VCs (hi, Chris!) asked just last week about what to charge for an SPV because he couldn’t find meaningful data on the topic either.

As Tom Magliozzi once said, “happiness is reality minus expectations,” so we want to do our part in sharing what reality looks like so you can adjust your expectations and (I hope!) be happier for it.

To get this data, we partnered with Assure, the Salt Lake City-based fund administrator founded in 2012, and platform to over 5,000 funds, which makes it the #3 largest fund admin in the world by fund-count (by contrast, the #2 spot is held by State Street, which was founded in 1792).

No Lack Of Reasons for Emerging VCs And LPs To Co-Invest

Here are a few more data points on why co-investing in emerging VC should be interesting:

It worked in PE

If you have been paying attention, you have already seen the countless articles and reports covering the rise and benefits of co-investing in private equity, but haven’t found much on co-investing in early-stage VC, much less any with statistically significant data.

It’s working for experienced LPs in VC

Cendana and Industry Ventures are two of the most prominent platforms that have been investing in and alongside emerging strategies for over a decade, and - using growth in AUM as a measure of customer happiness - appear to be resonating with LPs.

Complementarity sets the foundation for partnership

According to a recent survey of family offices, VC funds offer what family offices believe they need to run a successful VC program. Although “co-investment opportunities” was the #4 choice among respondents (see below), the top-3 motivations all describe the critical components of what co-investments offer. One could infer that family offices actually want to co-invest more, but are reluctant because they lack the information or resources to do it efficiently.

It’s working for VCs too

Tribe Capital saw enough of an opportunity in private, early-stage co-investing to acquire another VC firm and task them with productizing it:

Winter recently referred to this combination of blind pool and co-investing for emerging VCs as a “blurry vision pool,” whereby LPs get more discretion over investment decisions, and VCs can build AUM and conviction against otherwise unused pro rata into their best portfolio companies:

Pro rata can be a valuable asset

Like direct investing, the co-investing opportunities that pro rata offers are not automatic winners; but better to have the “call option” than not in case the conditions are right.

If planned to invest in top Series A deals, I would prefer to avoid competing with Sequoia for allocation, and instead come to the party with a reservation. The emerging VCs that are likely to front-run top firms like Sequoia may be able to provide me with that access:

The data

The following data comes from 5,500 SPVs structured and administered by Assure between 2012 - 2020, both through independently organized deals and via channel partnerships with platforms such as AngelList and Republic.

Note that some of these platform partners may have a say on SPV terms, which may skew the data to be more representative of these platforms’ terms rather than SPVs purely “in the wild.”

Observation: SPVs can let VCs and LPs ‘date before getting married’

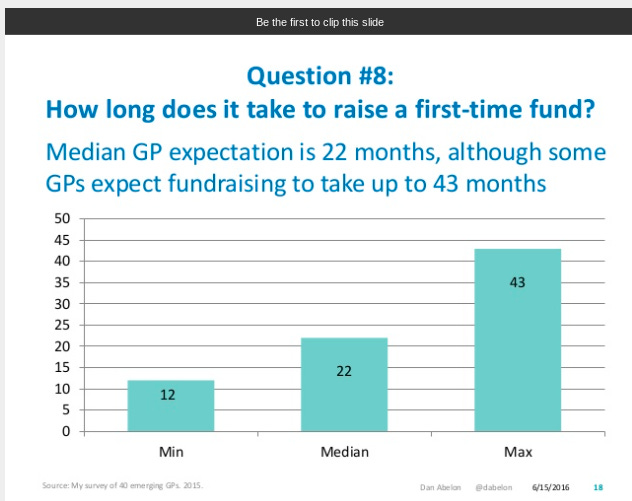

Raising a first-time (bind pool) fund can take really long time:

Compared to the median of >650 days to raise a blind pool, 26 days to close an SPV should look very attractive to a VC - or an LP - that isn’t ready to commit to a potentially very long and intensive process that comes with meaningful uncertainty when it comes to understanding which assets will end up in the portfolio.

Observation: Co-investing can help VCs and LPs solve for different outcomes

A blind pool can also involve many LPs, even for a smaller fund. Hustle Fund famously raised $11.5M from 90 LPs for its first fund, with an average check-size of about $128K. By contrast, the average SPV has 20 LPs with an average check-size of $68K, which implies less complexity for the VC (many fewer LPs), and a lower hurdle for the LP (smaller commitment).

Why the difference? From one VC’s perspective, the nature of committing to an SPV vs. a blind pool is fundamentally different for LPs:

“The difference between raising money for an SPV vs. for a fund, is that in an SPV the investor is underwriting the asset (the thing you are about to invest in), whereas in a fund, they are underwriting YOU”

Observation: Co-investing is still primarily a side-gig

Although at least one VC appears to be an SPV machine, running up to 157 SPVs in a single year (that’s 3 per week!) just on Assure, it appears that most VCs are normally running 1 SPV per year, which tells me that co-investing isn’t a core business.

Observation: “You can’t earn a salary by managing SPVs”

The averages of 1.2% for management fee, and 11.9% for carry (note: these are independent, not paired) are smaller than what’s normally budgeted for a micro-VC, indicating that co-investing is still largely a supplemental business, and co-investments are a feature that VCs can offer to their existing LPs.

Observation: You can earn a salary by managing SPVs

I found it surprising that the maximum carry fee has been 20% given that SPVs provide LPs with the unique benefit - relative to a blind pool - of having full knowledge of the asset before committing.

On the other hand, the maximum management fee of 4% tells me that at least one LP was willing to tolerate above-market rates to get into a deal (perhaps the LP was not in the VC’s fund, so was paying a premium for access to one of the VC’s standout portfolio companies).

Observation: Fees are a touchy issue, and always need context

Although the averages give a good starting-point for VCs and LPs to negotiate, they should consider the circumstances of the deal, including the nature of the relationship between the VC and LP, the value each party brings to the deal, and the deal itself.

It’s clear that fees can have a significant impact on returns - especially in VC - for all parties to the deal, so VCs and LPs should be thoughtful about finding the right alignment.

This topic deserves a lot more space than this article allows, so I’ll leave links to relevant articles in the section on Further Reading.

Suggestions

Consider doing more co-investing!

Make it easy for yourself - use a platform like Assure to help

Consider co-investing as it relates to LPA by accommodating co-investing, and maintaining GP/LP alignment: https://thefundlawyer.cooley.com/presentment-obligations-spvs-top-up/

LPs that are reluctant to commit to a fund may consider co-investing as a bridge, e.g. stapling co-investments to a fund commitment: https://teten.com/blog/2017/07/12/vcs-structure-syndicate-recruit-coinvestors/

VCs should consider “blurry vision pool” as a product, where co-investing is a prominent feature. This will affect other features of the fund, e.g. portfolio construction management as it relates to reserves

Topics to explore in the future include finding signal and avoiding adverse selection; how to find LPs for SPVs; fees

Further Reading

Crunchbase (data provider): How Pro Rata Works In Venture Capital Deals

Industry Ventures (LP): Small Funds and the Pro Rata Right

Blue Future Partners (LP): How much to charge for an SPV

SOP Ventures (VC): How VCs Can and Should Invest in Later Rounds

iAngels (VC): What To Know Before You Co-Invest

Cowboy Investing (LP): Part Time Venture Capital: What Could Go Wrong?

Companyon Ventures (VC): A Look Into Seed-Stage Venture Sidecar SPVs

IDO Investments (LP): The Issue with Co-Investment Fees in VC/PE Funds

Fin VC (VC): “Co-investment rights are critical…”

Kauffman Fellows (education program): Pitfalls LPs Need to Avoid When Co-Investing Directly in Startups

Cambridge Associates (investment firm): Ready, Steady, Co-Invest

Brooklyn Bridge Ventures (VC): How to Leverage Micro VC Funds to Build an Angel Portfolio

Assure (platform): Co-Investing with SPVs

Thank you to Jeremy Neilson (Assure) and team, John Hawthorne (Two Lanterns Venture Partners), and Nirav Bisarya (Gen3 Ventures) for contributing!

this is really useful

Great Insights!